| Filed by Lam Research Corporation Pursuant to Rule 425 under the Securities Act of 1933 and deemed filed pursuant to Rule 14a-12 under the Securities Exchange Act of 1934 Subject Company: KLA-Tencor Corporation Commission File No.: 000-09992 |

|

|

Lam Research + KLA-Tencor:

Creating a New Capability Paradigm

October 21, 2015

Lam Research Corp.

|

|

Cautions Regarding Forward-Looking Statements

All statements included or incorporated by reference in this document, other than statements or characterizations of historical fact, are forward-looking statements within the meaning of the federal securities laws, including Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements are based on Lam Research Corporation’s (“Lam”) and KLA-Tencor

Corporation’s (“KLA”) current expectations, estimates and projections about its respective business and industry, management’s beliefs, and certain assumptions made by Lam and KLA, all of which are subject to change. Forward-looking statements can often be identified by words such as

“anticipates,” “expects,” “intends,” “plans,” “predicts,” “believes,” “seeks,” “estimates,” “may,” “will,” “should,” “would,” “could,” “potential,” “continue,” “ongoing,” similar expressions, and variations or negatives of these words. Examples of such forward-looking statements include, but are not limited to: (1) references to the anticipated benefits of the proposed transaction; (2) the expected industry leadership, future technical capabilities and served markets of the individual and/or combined companies; (3) projections of pro forma revenue, cost synergies, revenue synergies, cash flow, market share and other metrics, whether by specific market segment, or as a whole, and whether for each individual company or the combined company; (4) market expansion opportunities and systems and products that may benefit from sales growth as a result of changes in market share or existing markets; (5) technological achievements that may be realized by the combined company, (6) the allocation of merger consideration in the transactions; (7) the financing components of the proposed transaction; (8) potential financing opportunities, together with sources and uses of cash; (9) potential dividend growth rates; (10) the companies’ ability to achieve the closing conditions and the expected date of closing of the transaction; (11) Lam’s expected revenue growth; (12) Lam’s ability to continue to successfully execute its growth strategy; (13) Lam’s ability to deliver growth and value for its customers and its stockholders; and (14) Lam’s guidance for shipments, revenue, gross margin, operating margin, earnings per share, and share count.

These forward-looking statements are not guarantees of future results and are subject to risks, uncertainties and assumptions that could cause actual results to differ materially and adversely from those expressed in any forward-looking statement. Important risk factors that may cause such a difference in connection with the proposed transaction include, but are not limited to, the following factors: (1) the risk that the conditions to the closing of the transaction are not satisfied, including the risk that required approvals for the transaction from governmental authorities or the stockholders of KLA or Lam are not obtained; (2) litigation relating to the transaction; (3) uncertainties as to the timing of the consummation of the transaction and the ability of each party to consummate the transaction; (4) risks that the proposed transaction disrupts the current plans and operations of KLA or Lam; (5) the ability of KLA and Lam to retain and hire key personnel; (6) competitive responses to the proposed transaction and the impact of competitive products; (7) unexpected costs, charges or expenses resulting from the transaction; (8) potential adverse reactions or changes to business relationships resulting from the announcement or completion of the transaction; (9) the combined companies’ ability to achieve the growth prospects and synergies expected from the transaction, as well as delays, challenges and expenses associated with integrating the combined companies’ existing businesses; (10) the terms and availability of the indebtedness planned to be incurred in connection with the transaction; and (11) legislative, regulatory and economic developments, including changing business conditions in the semiconductor industry and overall economy as well as the financial performance and expectations of Lam’s and KLA’s existing and prospective customers. These risks, as well as other risks associated with the proposed transaction, will be more fully discussed in the joint proxy statement/prospectus that will be included in the Registration Statement on Form

S-4 that Lam will file with the Securities and Exchange Commission (“SEC”) in connection with the proposed transaction. Investors and potential investors are urged not to place undue reliance on forward-looking statements in this document, which speak only as of this date. Neither Lam nor KLA undertakes any obligation to revise or update publicly any forward-looking statement to reflect future events or circumstances. Nothing contained herein constitutes or will be deemed to constitute a forecast, projection or estimate of the future financial performance of Lam, KLA, or the merged company, whether following the implementation of the proposed transaction or otherwise.

In addition, actual results are subject to other risks and uncertainties that relate more broadly to Lam’s overall business, including those more fully described in Lam’s filings with the SEC including its annual report on Form 10-K for the fiscal year ended June 28, 2015, and KLA’s overall business and financial condition, including those more fully described in KLA’s filings with the SEC including its annual report on Form 10-K for the fiscal year ended

June 30, 2015.

Lam Research Corp. 2

|

|

Additional Information and Where to Find It;

Participants in the Solicitation

Additional Information and Where to Find It:

This document does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. The proposed transaction will be submitted to the stockholders of each of Lam and KLA for their consideration. Lam intends to file with the SEC a Registration Statement on Form S-4 that will include a joint proxy statement/prospectus of Lam and KLA. Each of Lam and KLA will provide the joint proxy statement/prospectus to their respective stockholders. Lam and KLA also plan to file other documents with the SEC regarding the proposed transaction. This document is not a substitute for any prospectus, proxy statement or any other document that Lam or KLA may file with the SEC in connection with the proposed transaction. Investors and security holders of Lam and KLA are urged to read the joint proxy statement/prospectus and any other relevant documents that will be filed with the SEC carefully and in their entirety when they become available because they will contain important information about the proposed transaction. You may obtain copies of all documents filed with the SEC regarding this transaction, free of charge, at the SEC’s website (www.sec.gov). In addition, investors and stockholders will be able to obtain free copies of the joint proxy statement/prospectus and other documents filed with the SEC by Lam on Lam’s Investor Relations website (investor.lamresearch.com) or by writing to Lam Research Corporation, Investor Relations, 4650 Cushing Parkway, Fremont, CA 94538-6401 (for documents filed with the SEC by Lam), or by KLA on KLA’s Investor Relations website

(ir.kla-tencor.com) or by writing to KLA-Tencor Corporation, Investor Relations, One Technology Drive, Milpitas, California 95035 (for documents filed with the SEC by KLA).

Participants in the Solicitation:

Lam, KLA, their respective directors, and certain of their respective executive officers, other members of management and employees, may, under SEC rules, be deemed to be participants in the solicitation of proxies from Lam and KLA stockholders in connection with the proposed transaction. Information regarding the persons who, under SEC rules, are or may be deemed to be participants in the solicitation of Lam and KLA stockholders in connection with the proposed transaction will be set forth in the joint proxy statement/prospectus when it is filed with the SEC. You can find more detailed information about Lam’s executive officers and directors in its definitive proxy statement filed with the SEC on September 21, 2015. You can find more detailed information about

KLA’s executive officers and directors in its definitive proxy statement filed with the SEC on September 24, 2015. Additional information about Lam’s executive officers and directors and KLA’s executive officers and directors will be provided in the above-referenced

Registration Statement on Form S-4 when it becomes available.

Lam Research Corp. 3

|

|

Strategically and Financially Compelling Combination

Combines industry leaders in wafer processing and process control Unmatched capability to solve customers’ most difficult challenges Accelerated innovation opportunities with increased scale Broadens market presence with diversity across industry segments Delivers significant cost and revenue synergies

Accretive to non-GAAP earnings and FCF per share in the first 12 months post closing

FCF = free cash flow

Lam Research Corp. 4

|

|

Transaction Summary

Consideration Per Share

Transaction Consideration

Leadership & Board of Directors

Approval Process & Expected Closing

| (1) |

|

Based on Lam Research closing price of $70.03 on October 20, 2015. |

KLA-Tencor stockholders to receive:

Cash;

Lam stock; or

A mix of $32.00 and 0.5 shares of Lam stock per share

Final election subject to a proration based on total transaction consideration

~$10.6B of total consideration for KLA-Tencor stockholders

~$5.0B in cash

~80M shares of Lam (current value of $5.6B(1))

KLA-Tencor stockholders expected to own ~32% of combined company

Martin Anstice, CEO

Steve Newberry, Chairman

Two new members added to the Lam Board from KLA-Tencor’s Board

Lam Research and KLA-Tencor stockholder approval Customary closing conditions and regulatory approvals

Estimate deal close in mid-CY 2016

Lam Research Corp. 5

|

|

The Right Combination at the Right Time

Cloud, mobility, and IoT are driving performance and economic requirements Technology scaling continues with escalating challenges Customer roadmaps require enhanced collaboration and innovation Intersection of process and process control becoming more critical Unmatched and complementary capability to enable atomic level processing

Accelerating our capability to address our customers’ most difficult challenges

Lam Research Corp. 6

|

|

Our Businesses at a Glance

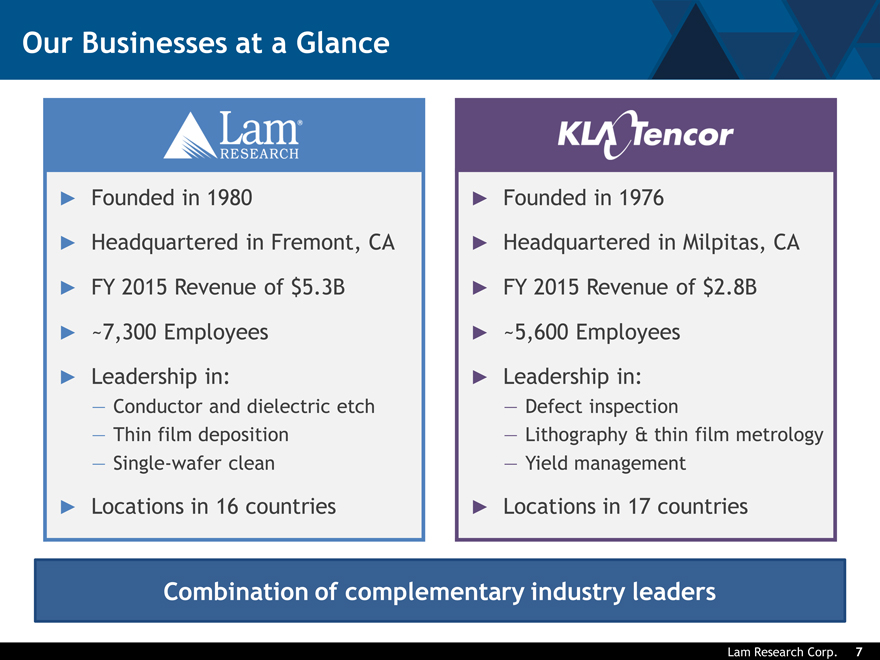

Founded in 1980

Headquartered in Fremont, CA FY 2015 Revenue of $5.3B ~7,300 Employees Leadership in:

— Conductor and dielectric etch

— Thin film deposition

— Single-wafer clean

Locations in 16 countries

Founded in 1976

Headquartered in Milpitas, CA FY 2015 Revenue of $2.8B ~5,600 Employees Leadership in:

— Defect inspection

— Lithography & thin film metrology

— Yield management

Locations in 17 countries

Combination of complementary industry leaders

Lam Research Corp. 7

|

|

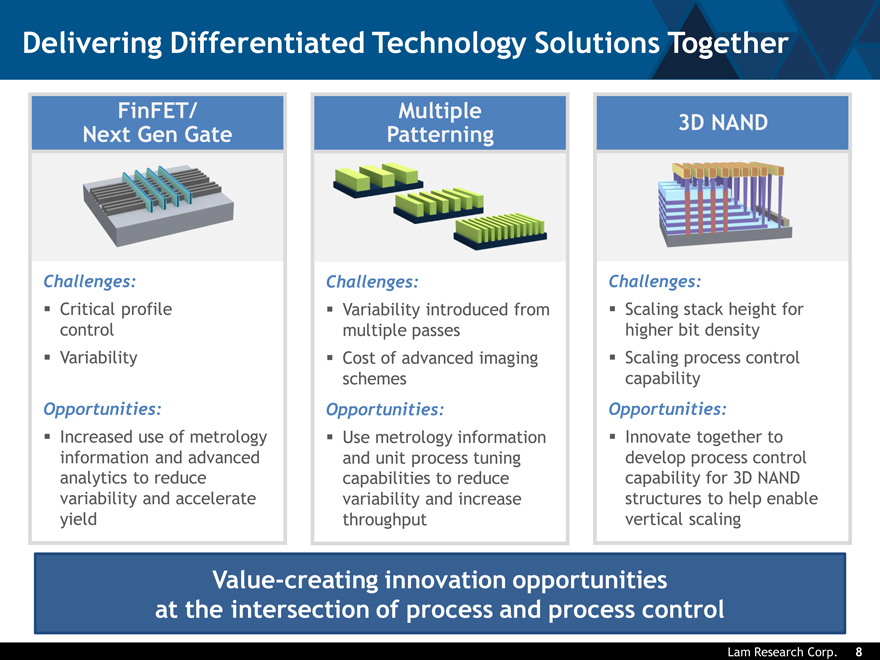

Delivering Differentiated Technology Solutions Together

FinFET/ Multiple

3D NAND

Next Gen Gate Patterning

Challenges: Challenges: Challenges:

Critical profile Variability introduced from Scaling stack height for control multiple passes higher bit density

Variability Cost of advanced imaging Scaling process control schemes capability

Opportunities: Opportunities: Opportunities:

? Increased use of metrology ? Use metrology information Innovate together to information and advanced and unit process tuning develop process control analytics to reduce capabilities to reduce capability for 3D NAND variability and accelerate variability and increase structures to help enable yield throughput vertical scaling

Value-creating innovation opportunities at the intersection of process and process control

Lam Research Corp. 8

|

|

Established Product Leadership

Deposition Etch Clean Inspection Metrology

in Wafer

#1 in Copper ECD #1 in Conductor #1 in Bevel Clean #1 #1 in Metrology Inspection in BEOL SW in Mask #1 in Tungsten CVD #2 in Dielectric #1 #1 Clean Inspection in Packaging #2 in PECVD & HDP #1 Inspection

#2 in ALD*

7% – 9% of WFE 14% – 16% of WFE 5% – 6% of WFE 6%—7% of WFE 6%—7% of WFE

Combined company to serve ~42% of WFE market upon closing, increasing to ~45% by 2018

Source: Leadership positions based on Gartner and company data specific to 2014 shares. WFE percentages are for 2015 markets based on Gartner and company data. ECD = electrochemical deposition, CVD = chemical vapor deposition, PECVD = plasma-enhanced CVD, HDP = high-density plasma (CVD), ALD = atomic layer deposition, BEOL = back-end-of-line, SW = single-wafer. *Based on year-over-year absolute revenue growth. WFE = wafer fabrication equipment

Lam Research Corp. 9

|

|

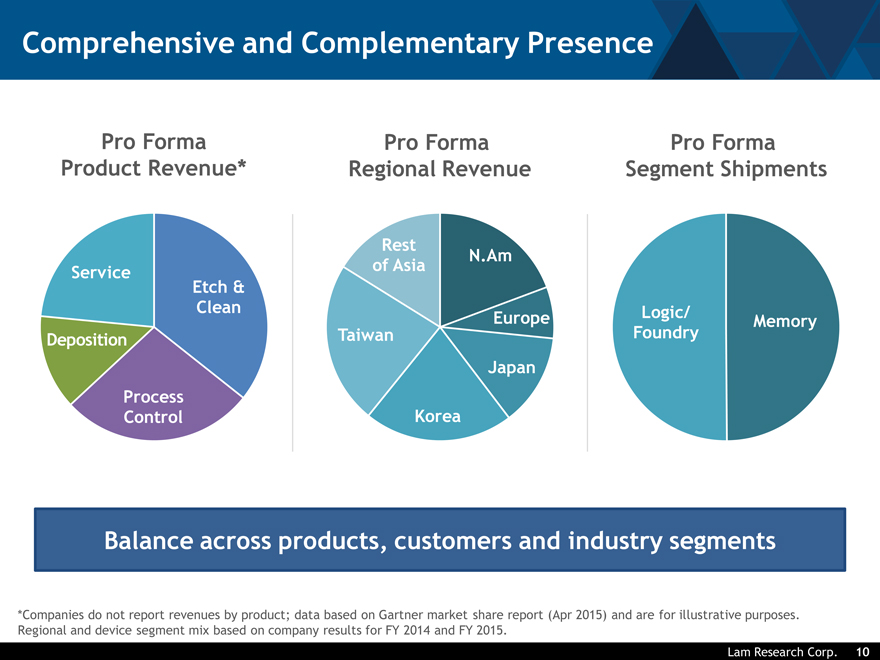

Comprehensive and Complementary Presence

Pro Forma Pro Forma Pro Forma Product Revenue* Regional Revenue Segment Shipments

Rest

N.Am Service of Asia Etch &

Clean Logic/

Europe Memory Deposition Taiwan Foundry

Japan Process

Control Korea

Balance across products, customers and industry segments

*Companies do not report revenues by product; data based on Gartner market share report (Apr 2015) and are for illustrative purposes. Regional and device segment mix based on company results for FY 2014 and FY 2015.

Lam Research Corp. 10

|

|

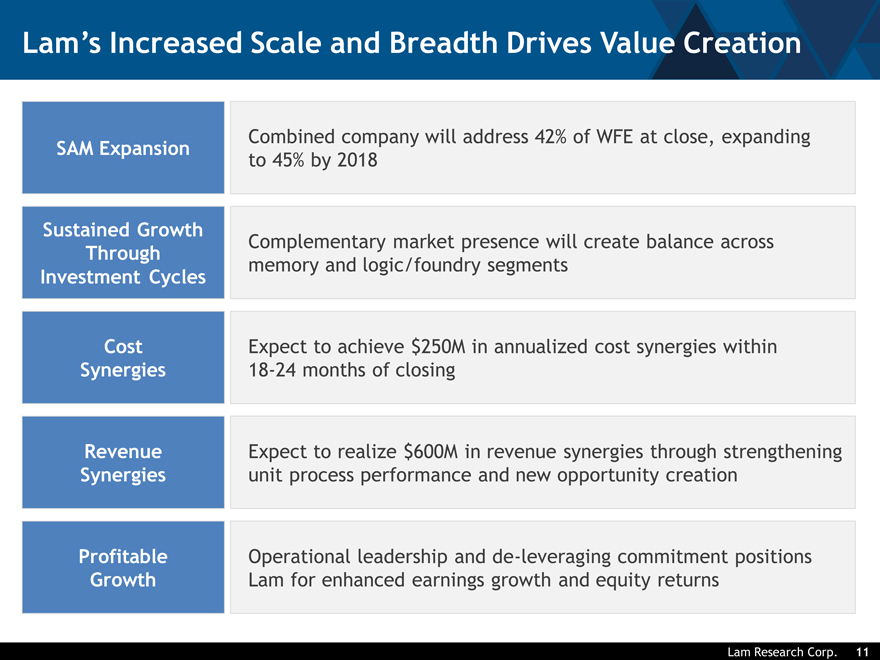

Lam’s Increased Scale and Breadth Drives Value Creation

Combined company will address 42% of WFE at close, expanding

SAM Expansion

to 45% by 2018

Sustained Growth

Complementary market presence will create balance across

Through

memory and logic/foundry segments

Investment Cycles

Cost Expect to achieve $250M in annualized cost synergies within

Synergies 18-24 months of closing

Revenue Expect to realize $600M in revenue synergies through strengthening

Synergies unit process performance and new opportunity creation

Profitable Operational leadership and de-leveraging commitment positions

Growth Lam for enhanced earnings growth and equity returns

Lam Research Corp. 11

|

|

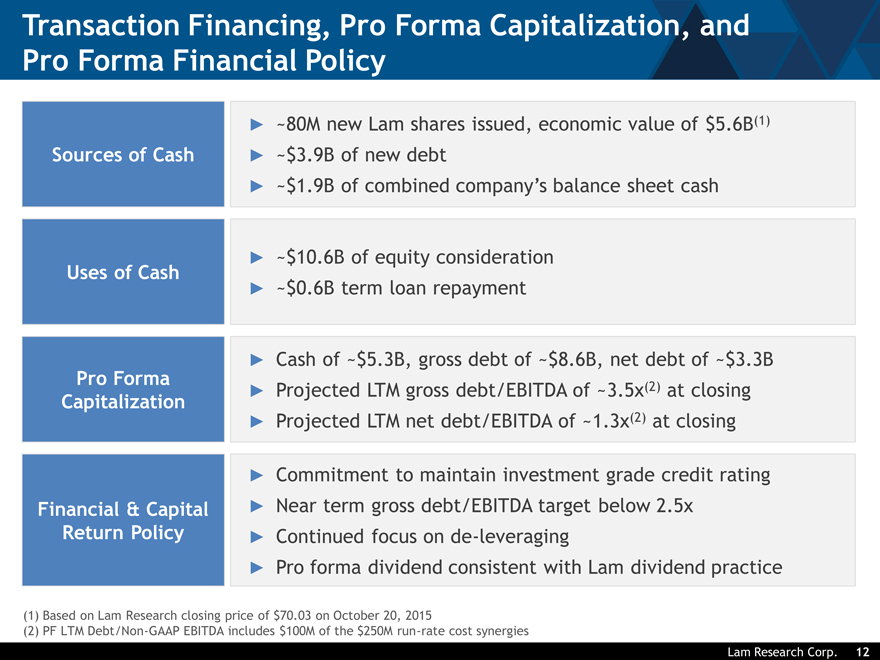

Transaction Financing, Pro Forma Capitalization, and Pro Forma Financial Policy

Sources of Cash

Uses of Cash

Pro Forma Capitalization

Financial & Capital Return Policy

(1) Based on Lam Research closing price of $70.03 on October 20, 2015

(2) PF LTM Debt/Non-GAAP EBITDA includes $100M of the $250M run-rate cost synergies

~80M new Lam shares issued, economic value of $5.6B(1)

~$3.9B of new debt

~$1.9B of combined company’s balance sheet cash

~$10.6B of equity consideration

~$0.6B term loan repayment

Cash of ~$5.3B, gross debt of ~$8.6B, net debt of ~$3.3B Projected LTM gross debt/EBITDA of ~3.5x(2) at closing Projected LTM net debt/EBITDA of ~1.3x(2) at closing

Commitment to maintain investment grade credit rating Near term gross debt/EBITDA target below 2.5x Continued focus on de-leveraging Pro forma dividend consistent with Lam dividend practice

Lam Research Corp. 12

|

|

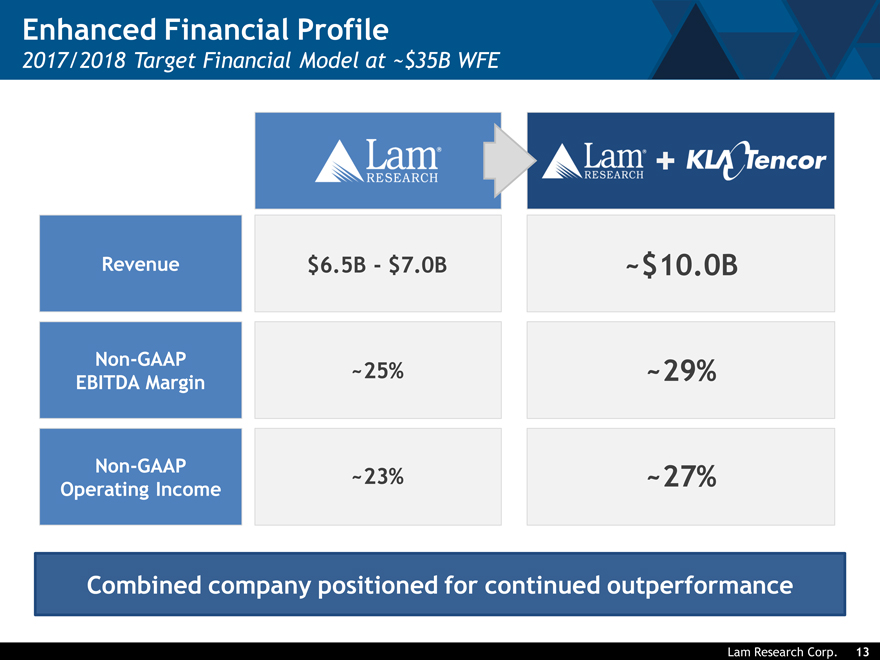

Enhanced Financial Profile

2017/2018 Target Financial Model at ~$35B WFE

Revenue $6.5B—$7.0B ~$10.0B

Non-GAAP

~25% ~29%

EBITDA Margin

Non-GAAP ~23% ~27% Operating Income

Combined company positioned for continued outperformance

Lam Research Corp. 13

|

|

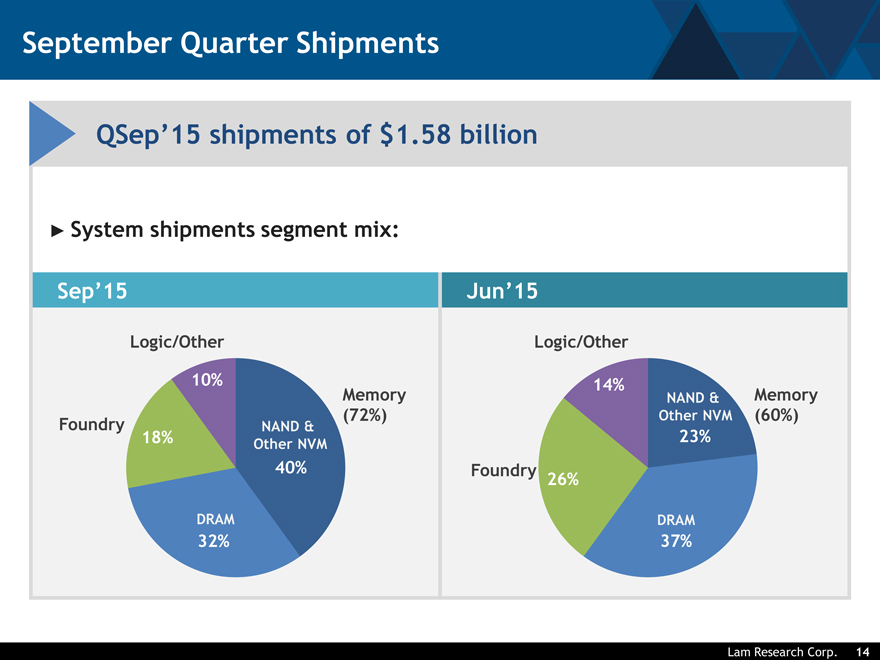

September Quarter Shipments

QSep’15 shipments of $1.58 billion

System shipments segment mix:

Sep’15 Jun’15

Logic/Other Logic/Other

10% 14%

Memory NAND & Memory (72%) Other NVM (60%) Foundry NAND &

18% Other NVM 23%

40% Foundry 26%

DRAM DRAM

32% 37%

Lam Research Corp. 14

|

|

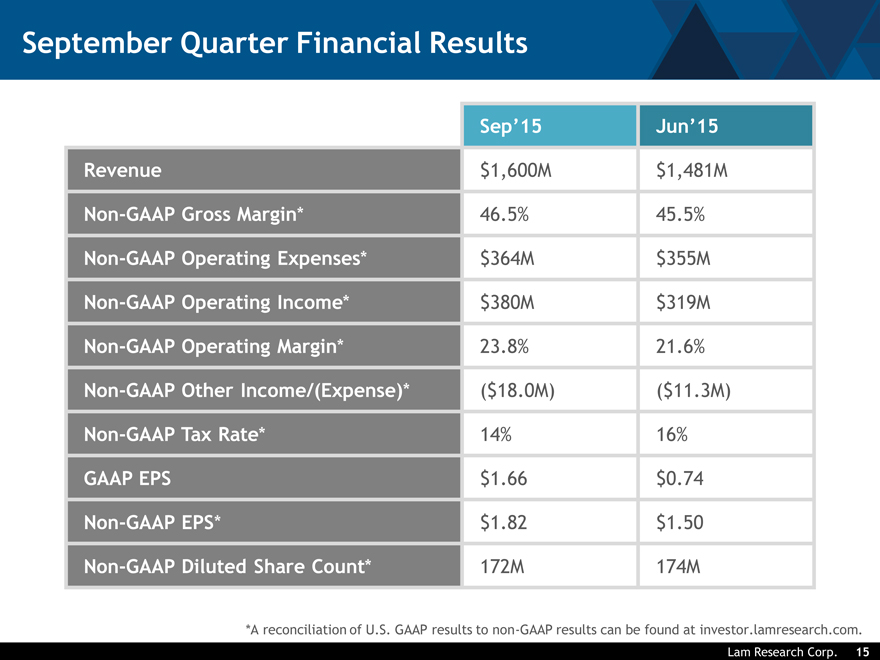

September Quarter Financial Results

Sep’15 Jun’15

Revenue $1,600M $1,481M

Non-GAAP Gross Margin* 46.5% 45.5%

Non-GAAP Operating Expenses* $364M $355M

Non-GAAP Operating Income* $380M $319M

Non-GAAP Operating Margin* 23.8% 21.6%

Non-GAAP Other Income/(Expense)*($18.0M)($11.3M)

Non-GAAP Tax Rate* 14% 16%

GAAP EPS $1.66 $0.74

Non-GAAP EPS* $1.82 $1.50

Non-GAAP Diluted Share Count* 172M 174M

*A reconciliation of U.S. GAAP results to non-GAAP results can be found at investor.lamresearch.com.

Lam Research Corp. 15

|

|

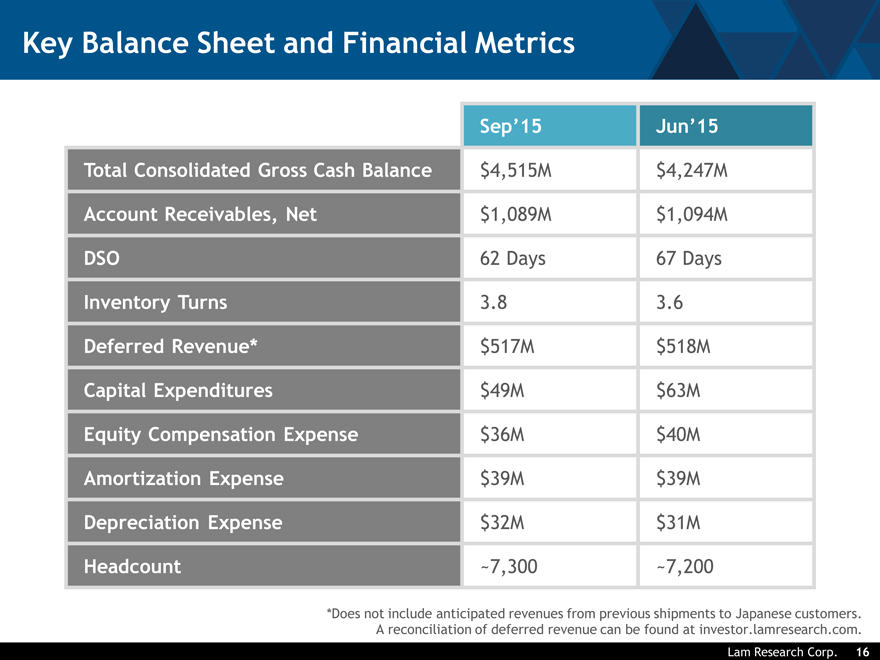

Key Balance Sheet and Financial Metrics

Sep’15 Jun’15

Total Consolidated Gross Cash Balance $4,515M $4,247M

Account Receivables, Net $1,089M $1,094M

DSO 62 Days 67 Days

Inventory Turns 3.8 3.6

Deferred Revenue* $517M $518M

Capital Expenditures $49M $63M

Equity Compensation Expense $36M $40M

Amortization Expense $39M $39M

Depreciation Expense $32M $31M

Headcount ~7,300 ~7,200

*Does not include anticipated revenues from previous shipments to Japanese customers.

A reconciliation of deferred revenue can be found at investor.lamresearch.com.

Lam Research Corp. 16

|

|

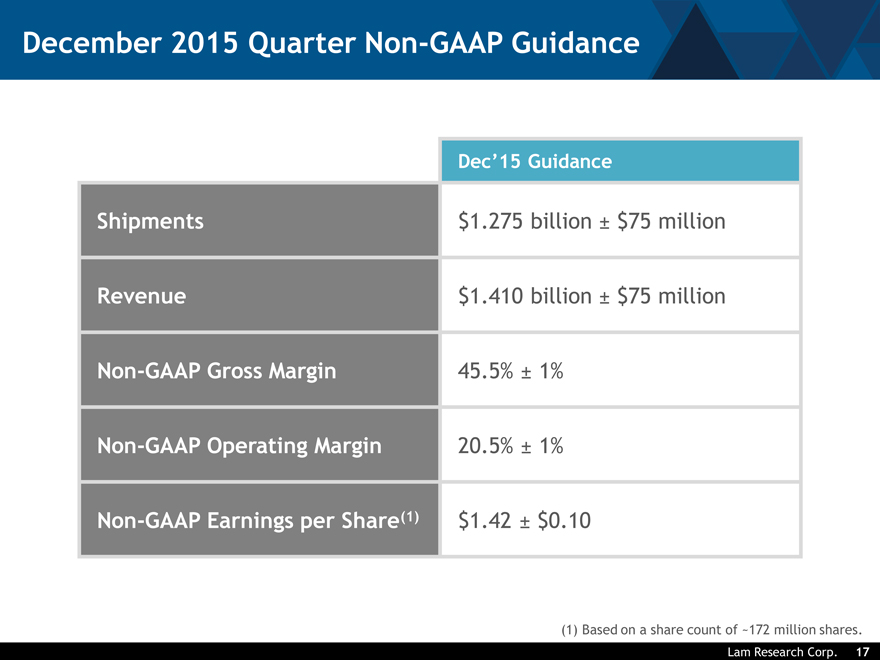

December 2015 Quarter Non-GAAP Guidance

Dec’15 Guidance

Shipments $1.275 billion ± $75 million

Revenue $1.410 billion ± $75 million

Non-GAAP Gross Margin 45.5% ± 1%

Non-GAAP Operating Margin 20.5% ± 1%

Non-GAAP Earnings per Share(1) $1.42 ± $0.10

| (1) |

|

Based on a share count of ~172 million shares. |

Lam Research Corp. 17

|

|

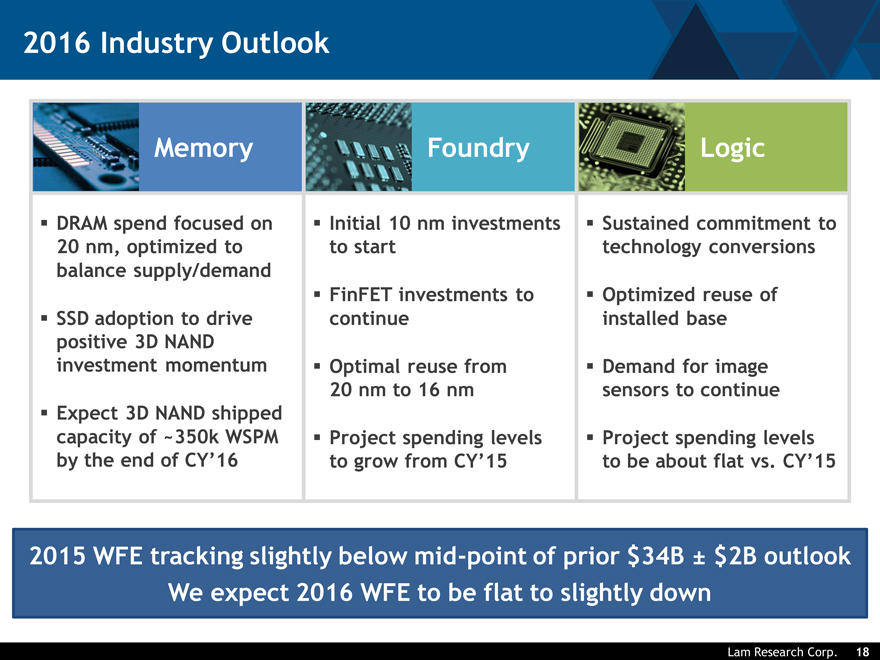

2016 Industry Outlook

DRAM spend focused on 20 nm, optimized to balance supply/demand

SSD adoption to drive positive 3D NAND investment momentum

Expect 3D NAND shipped capacity of ~350k WSPM by the end of CY’16

Initial 10 nm investments to start

FinFET investments to continue

Optimal reuse from 20 nm to 16 nm

Project spending levels to grow from CY’15

Sustained commitment to technology conversions

Optimized reuse of installed base

Demand for image sensors to continue

Project spending levels to be about flat vs. CY’15

Memory Foundry Logic

2015 WFE tracking slightly below mid-point of prior $34B ± $2B outlook We expect 2016 WFE to be flat to slightly down

Lam Research Corp. 18

|

|

KLA-Tencor

Q1 FY16 Financial Results and Q2 FY16 Outlook

Lam Research Corp. 19

|

|

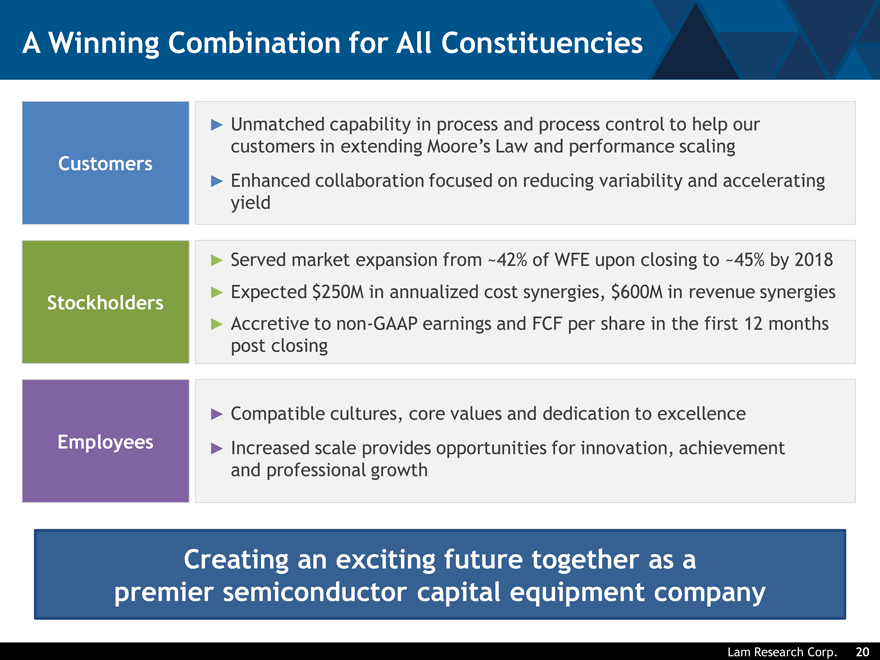

A Winning Combination for All Constituencies

Unmatched capability in process and process control to help our

Customers customers in extending Moore’s Law and performance scaling

Enhanced collaboration focused on reducing variability and accelerating yield

Served market expansion from ~42% of WFE upon closing to ~45% by 2018

Expected $250M in annualized cost synergies, $600M in revenue synergies

Stockholders

Accretive to non-GAAP earnings and FCF per share in the first 12 months post closing

Compatible cultures, core values and dedication to excellence

Employees Increased scale provides opportunities for innovation, achievement and professional growth

Creating an exciting future together as a premier semiconductor capital equipment company

Lam Research Corp. 20

|

|

Lam research

|

|

Appendix – Reconciliation

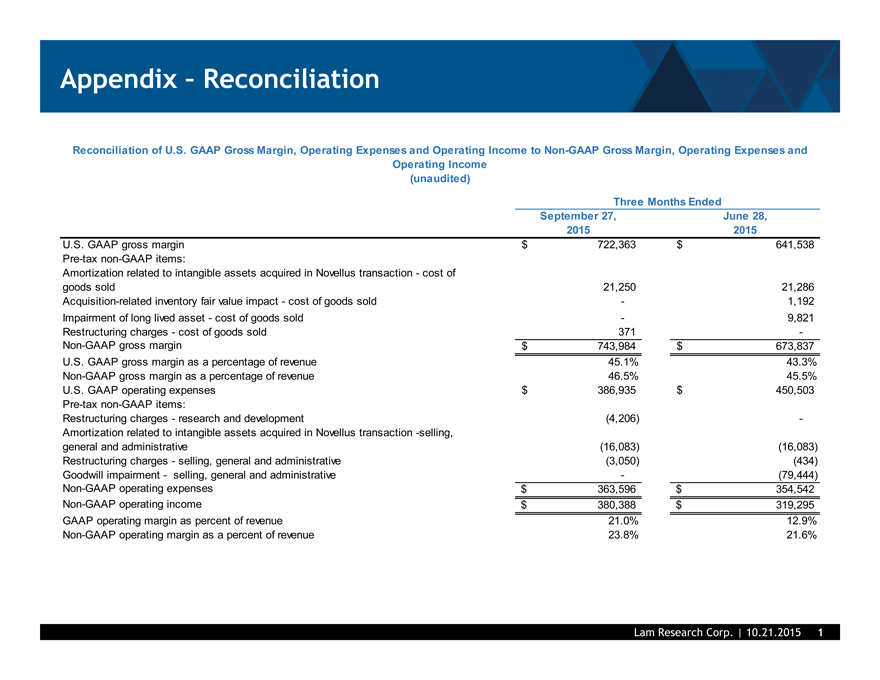

Reconciliation of U.S. GAAP Gross Margin, Operating Expenses and Operating Income to Non-GAAP Gross Margin, Operating Expenses and Operating Income (unaudited)

Three Months Ended

September 27, June 28, 2015 2015

U.S. GAAP gross margin $ 722,363 $ 641,538 Pre-tax non-GAAP items: Amortization related to intangible assets acquired in Novellus transaction—cost of goods sold 21,250 21,286 Acquisition-related inventory fair value impact—cost of goods sold — 1,192 Impairment of long lived asset—cost of goods sold — 9,821 Restructuring charges—cost of goods sold 371 -Non-GAAP gross margin $ 743,984 $ 673,837 U.S. GAAP gross margin as a percentage of revenue 45.1% 43.3% Non-GAAP gross margin as a percentage of revenue 46.5% 45.5% U.S. GAAP operating expenses $ 386,935 $ 450,503 Pre-tax non-GAAP items: Restructuring charges—research and development (4,206) -Amortization related to intangible assets acquired in Novellus transaction -selling, general and administrative (16,083) (16,083) Restructuring charges—selling, general and administrative (3,050) (434) Goodwill impairment— selling, general and administrative — (79,444) Non-GAAP operating expenses $ 363,596 $ 354,542 Non-GAAP operating income $ 380,388 $ 319,295 GAAP operating margin as percent of revenue 21.0% 12.9% Non-GAAP operating margin as a percent of revenue 23.8% 21.6%

Lam Research Corp. | 10.21.2015 1

|

|

Appendix – Reconciliation

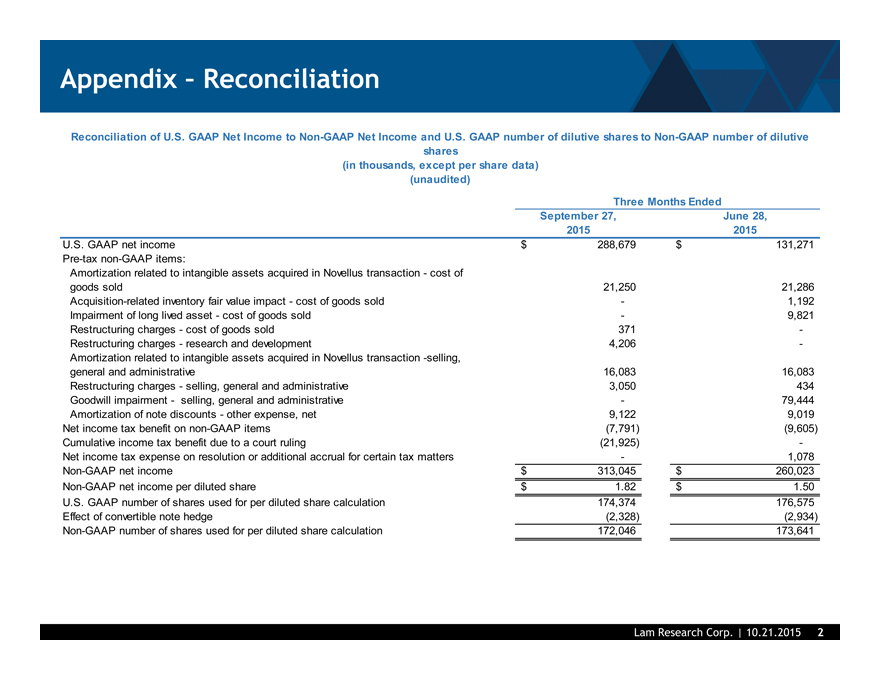

Reconciliation of U.S. GAAP Net Income to Non-GAAP Net Income and U.S. GAAP number of dilutive shares to Non-GAAP number of dilutive shares (in thousands, except per share data) (unaudited)

Three Months Ended

September 27, June 28, 2015 2015

U.S. GAAP net income $ 288,679 $ 131,271 Pre-tax non-GAAP items: Amortization related to intangible assets acquired in Novellus transaction—cost of goods sold 21,250 21,286 Acquisition-related inventory fair value impact—cost of goods sold — 1,192 Impairment of long lived asset—cost of goods sold — 9,821 Restructuring charges—cost of goods sold 371 -Restructuring charges—research and development 4,206 -Amortization related to intangible assets acquired in Novellus transaction -selling, general and administrative 16,083 16,083 Restructuring charges—selling, general and administrative 3,050 434 Goodwill impairment— selling, general and administrative — 79,444 Amortization of note discounts—other expense, net 9,122 9,019 Net income tax benefit on non-GAAP items (7,791) (9,605) Cumulative income tax benefit due to a court ruling (21,925) -Net income tax expense on resolution or additional accrual for certain tax matters — 1,078 Non-GAAP net income $ 313,045 $ 260,023 Non-GAAP net income per diluted share $ 1.82 $ 1.50 U.S. GAAP number of shares used for per diluted share calculation 174,374 176,575 Effect of convertible note hedge (2,328) (2,934) Non-GAAP number of shares used for per diluted share calculation 172,046 173,641

Lam Research Corp. | 10.21.2015 2

|

|

Appendix – Reconciliation

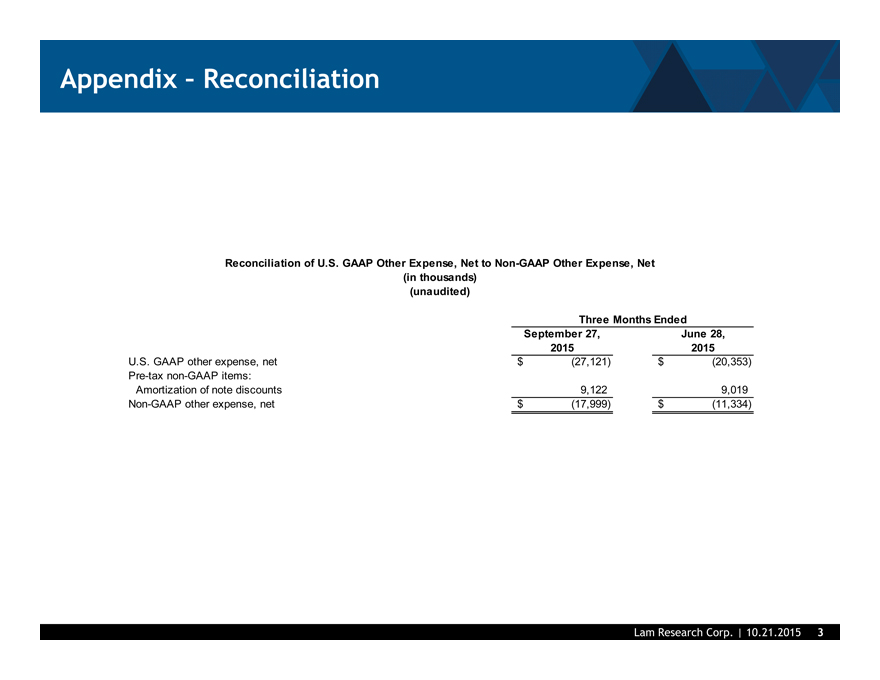

Reconciliation of U.S. GAAP Other Expense, Net to Non-GAAP Other Expense, Net (in thousands) (unaudited)

Three Months Ended September 27, June 28, 2015 2015

U.S. GAAP other expense, net $ (27,121) $ (20,353) Pre-tax non-GAAP items: Amortization of note discounts 9,122 9,019 Non-GAAP other expense, net $ (17,999) $ (11,334)

Lam Research Corp. | 10.21.2015 3

|

|

Appendix – Reconciliation

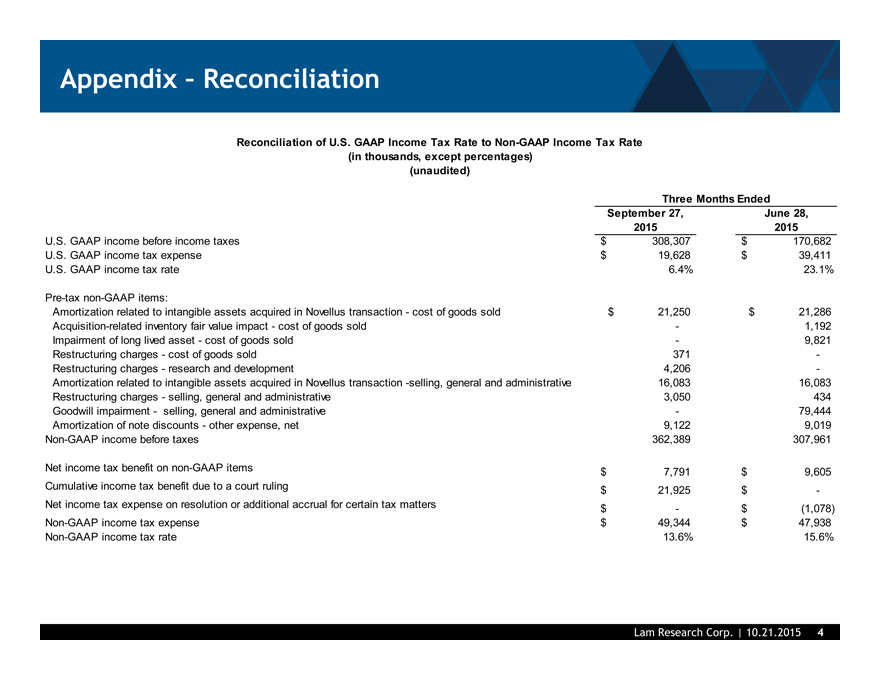

Reconciliation of U.S. GAAP Income Tax Rate to Non-GAAP Income Tax Rate (in thousands, except percentages) (unaudited)

Three Months Ended September 27, June 28, 2015 2015

U.S. GAAP income before income taxes $ 308,307 $ 170,682 U.S. GAAP income tax expense $ 19,628 $ 39,411 U.S. GAAP income tax rate 6.4% 23.1%

Pre-tax non-GAAP items:

Amortization related to intangible assets acquired in Novellus transaction—cost of goods sold $ 21,250 $ 21,286 Acquisition-related inventory fair value impact—cost of goods sold — 1,192 Impairment of long lived asset—cost of goods sold — 9,821 Restructuring charges—cost of goods sold 371 -Restructuring charges—research and development 4,206 -Amortization related to intangible assets acquired in Novellus transaction -selling, general and administrative 16,083 16,083 Restructuring charges—selling, general and administrative 3,050 434 Goodwill impairment— selling, general and administrative — 79,444 Amortization of note discounts—other expense, net 9,122 9,019 Non-GAAP income before taxes 362,389 307,961

Net income tax benefit on non-GAAP items $ 7,791 $ 9,605 Cumulative income tax benefit due to a court ruling $ 21,925 $ -Net income tax expense on resolution or additional accrual for certain tax matters $ —$ (1,078) Non-GAAP income tax expense $ 49,344 $ 47,938 Non-GAAP income tax rate 13.6% 15.6%

Lam Research Corp. | 10.21.2015 4

|

|

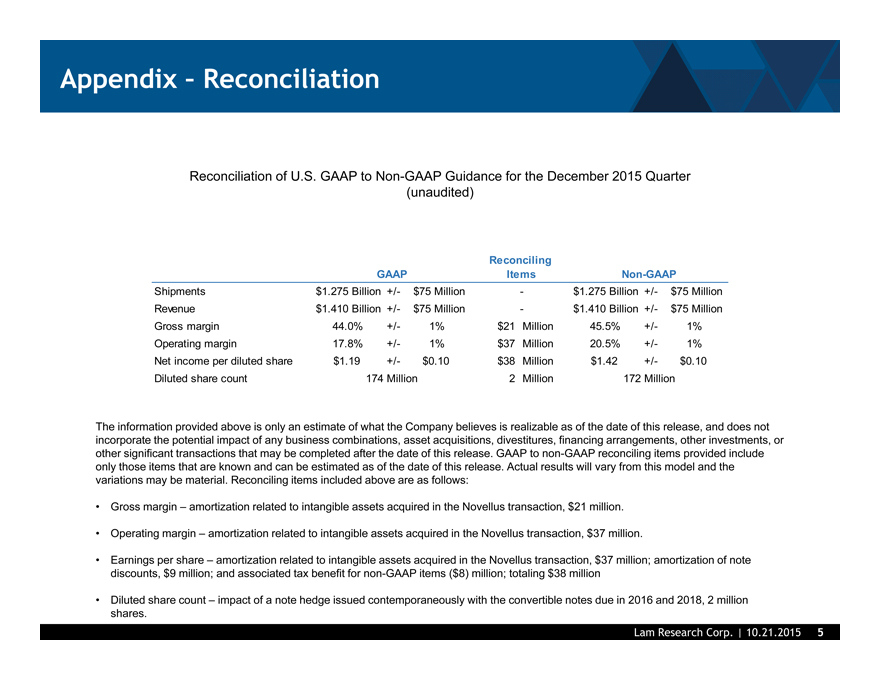

Appendix – Reconciliation

Reconciliation of U.S. GAAP to Non-GAAP Guidance for the December 2015 Quarter (unaudited)

Reconciling

GAAP Items Non-GAAP

Shipments $1.275 Billion +/- $75 Million—$1.275 Billion +/- $75 Million Revenue $1.410 Billion +/- $75 Million—$1.410 Billion +/- $75 Million Gross margin 44.0% +/- 1% $21 Million 45.5% +/- 1% Operating margin 17.8% +/- 1% $37 Million 20.5% +/- 1% Net income per diluted share $1.19 +/- $0.10 $38 Million $1.42 +/- $0.10 Diluted share count 174 Million 2 Million 172 Million

The information provided above is only an estimate of what the Company believes is realizable as of the date of this release, and does not incorporate the potential impact of any business combinations, asset acquisitions, divestitures, financing arrangements, other investments, or other significant transactions that may be completed after the date of this release. GAAP to non-GAAP reconciling items provided include only those items that are known and can be estimated as of the date of this release. Actual results will vary from this model and the variations may be material. Reconciling items included above are as follows:

Gross margin – amortization related to intangible assets acquired in the Novellus transaction, $21 million.

Operating margin – amortization related to intangible assets acquired in the Novellus transaction, $37 million.

Earnings per share – amortization related to intangible assets acquired in the Novellus transaction, $37 million; amortization of note discounts, $9 million; and associated tax benefit for non-GAAP items ($8) million; totaling $38 million

Diluted share count – impact of a note hedge issued contemporaneously with the convertible notes due in 2016 and 2018, 2 million shares.

Lam Research Corp. | 10.21.2015 5

|

|

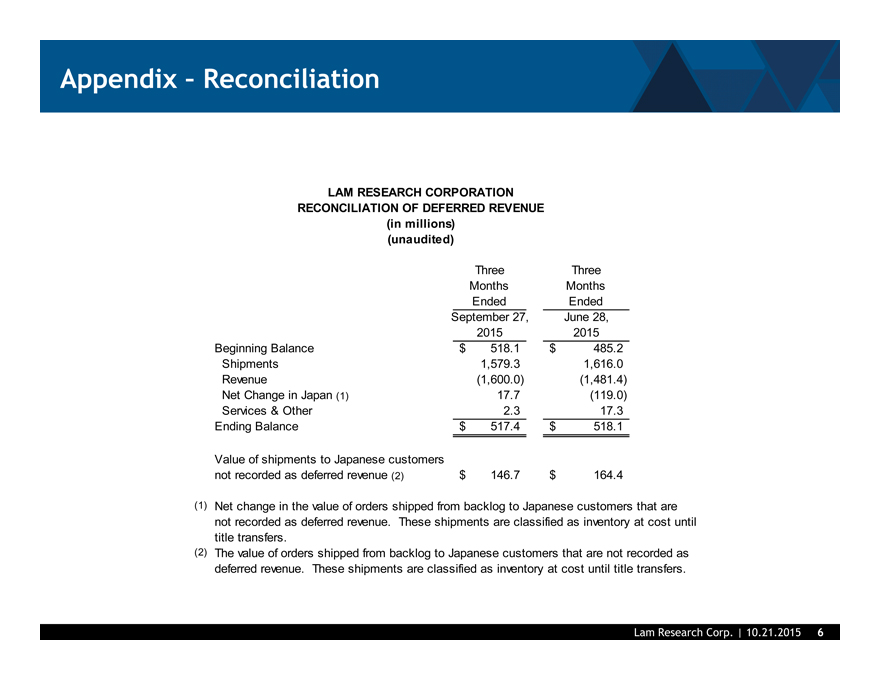

Appendix – Reconciliation

LAM RESEARCH CORPORATION RECONCILIATION OF DEFERRED REVENUE

(in millions) (unaudited)

Three Three Months Months Ended Ended September 27, June 28, 2015 2015 Beginning Balance $ 518.1 $ 485.2 Shipments 1,579.3 1,616.0 Revenue (1,600.0) (1,481.4) Net Change in Japan (1) 17.7 (119.0) Services & Other 2.3 17.3 Ending Balance $ 517.4 $ 518.1

Value of shipments to Japanese customers not recorded as deferred revenue (2) $ 146.7 $ 164.4

(1) Net change in the value of orders shipped from backlog to Japanese customers that are not recorded as deferred revenue. These shipments are classified as inventory at cost until title transfers.

(2) The value of orders shipped from backlog to Japanese customers that are not recorded as deferred revenue. These shipments are classified as inventory at cost until title transfers.

Lam Research Corp. | 10.21.2015 6